Round up of China's 2024 work report

No major surprises on supply vs demand priorities or the property sector, but interesting to see strong focus on education and willingness to abandon the hukou system

We need to stop calling it an ambitious growth target

First a bit of housekeeping. Chinese GDP growth is largely politically determined, not so much driven by the underlying forces of the real economy – such as private consumption, business investment and net exports. The GDP growth target (which always is met) is set to enable policymakers to meet other KPIs, such as job creation and poverty alleviation. For instance, Beijing has determined that it needs around 5% GDP growth to create around 12m jobs. China, like any other country, can set and meet whatever GDP growth target (within reason) that it wants if it is willing and able to borrow and invest sufficiently. Beijing has been setting GDP growth targets that are higher than what the “real economy” can produce for the last 15 years or so – filling the gap with unproductive investment in infrastructure, property and increasingly manufacturing capacity. This is why debt as a share of GDP has morphed since then. So if this year’s growth target is ambitious, then GDP growth targets since around 2008 should also be described as ambitious.

More evidence of local governments being stripped of their powers

In my previous newsletter I argued that there is real evidence which suggests that Beijing is sincere about moving away from its investment-led growth model – even if it leads to slower headline GDP growth. I said this is partly made possible by stripping local governments of control over how they spend their funds. The work report indicates that this process will be intensified, noting that the investment approval system will see further reform, that Beijing will guard against wasteful investment and that a pool of 700bn RMB earmarked for investment will be weighted toward regions “where projects are well-prepared and investments are more effective.” This is arguably a very positive development.

Not much support for households and domestic demand, but some positives can be found

Unfortunately, as the government work report showed today, there is also evidence which suggests that Beijing is some way off taking real steps to boost the part of the economy that constantly is lagging – namely household demand. While investment in public housing (see below) is welcome news as it will function as a transfer to low-income households – allowing them to consume more of their income – doubling down on state support for the manufacturing sector (see below) works the other way as it directs public resources away from households and keeps a lid on wage growth. The latter unfortunately being necessary to protect industrial competitiveness.

While it should be noted that the report says more will be done to increase people’s income, it offers few details on how it will be done. The section on expanding domestic demand also mainly focuses on how the government will “develop new types of consumption” and how it will make it easier to consume – by reducing restrictions (not sure what those are) and improving supply of goods and services. As if lack of supply is a constraint on consumption in China.

The report also highlights President Xi Jinping’s grand consumer goods trade-in scheme, which he laid out during a recent meeting of the Central Financial and Economic Affairs Commission – and which he believes will boost consumption and promote “high quality development”. This is quite worrisome as issuing vouchers and offering discounts to encourage households to replace old consumer goods with new only will generate a small boost for some sectors and is really just a way of dealing with oversupply. Moreover, if wealthy Shanghai can offer no more than 10,000 RMB in EV subsidies and 10% off the price of home appliances, then it is unlikely that the scheme will be particularly effective on a national basis.

On a more positive note, the report basically says that the central government intends to get rid of the hukou – or household registration system – which is blocking workers without a hukou from accessing public services in the cities they live and work in. If this were to happen, it would allow millions of migrant workers to consume more and save less of their income. The challenge, of course, is to get local officials – who need to fund the public services – to comply. Given declining local government revenue, successful implementation would likely require a sharp increase in central transfers.

Relatedly, the report says parental leave policies will be improved in terms of length and pay, and that the government will boost the supply of childcare services. This, combined with improving access to and the quality of education (listed in the report as priority task number 2!) would be important steps in terms of strengthening basic public services. Still, as with hukou reform, the impact will depend on whether words get translated into action.

Unleashing the new productive forces

Strengthening China’s industrial base was unsurprisingly listed as priority number one for 2024, with developing “new quality productive forces” – currently Xi’s favourite phrase – highlighted at the very top. While not much new was mentioned in terms of priorities and policy support – resembling local government work reports from January and the Central Economic Work Conference readout from December – the focus on manufacturing and technological breakthroughs highlight at least three major concerns.

Raising total factor productivity (explicitly mentioned in the report) is needed as capital and labour will contribute little (or even negatively) to growth going forward.

Alternative manufacturing hubs are knocking on China’s door, threatening to chip away at its share of global manufacturing. This concern also explains why Xi recently made a big point about lowering logistics costs. Other countries have lower labour costs, but China is still unrivalled when it comes to logistics. It needs to protect this advantage.

Worsening geopolitical tensions with the US and its allies will lead to tighter overseas supply of high-tech goods that China cannot produce itself at this point. This also explains the work report’s focus on education and skills.

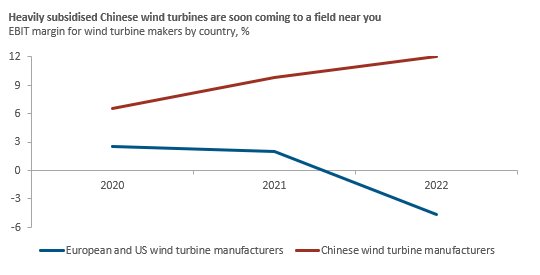

Ultimately, it seems clear that we should expect to see another monstrous wave of state support for priority industries in the high-tech and renewables space, as well as for the manufacturing sector more broadly. Indeed, in addressing the need to keep employment stable, the report said more support will be provided to “sectors and enterprises with a large capacity for creating jobs”. That clearly includes the manufacturing sector, and will together with promises of more support to boost foreign trade have an adverse impact relations with the US and EU in particular.

No change in real estate policy

Some analysts have pointed to the omission of “houses are for living in, not for speculation”, arguing that it signals more support for the property sector. I don’t believe this phrase matters anymore. Local officials have been actively encouraging speculation in the property market for the last two years. But it has had little effect because the overarching message coming out of Beijing is to “foster a new development model” for the real estate sector that focuses on providing affordable housing for the people through subsidies or lower prices – even if the latter is not explicitly mentioned. This messaging was repeated in the report, signalling no change in approach.

Market implications

The market implications section was omitted by accident from last week’s newsletter. So, I have included them in this post.

Sincere focus on scaling back investment underscores that growth will be slower in the years to come. Xi’s new productive forces cannot replace property and infrastructure as drivers for growth.

The slowdown and its impact on wage growth and the labour market is impacting consumer preferences, who increasingly are buying budget over premium brands. This will negatively impact foreign brands more than domestic. Domestic brands will also benefit from subsidies and the consumer goods trade-in campaign.

Chinese demand for commodities will also not recover to what it has been, leading to lower prices. There are also new efforts in China to increase domestic supply, which will push prices further down. The world’s largest copper mine was just approved by the NDRC.

Subdued Chinese demand, combined with increased commodities supply, should also offer some respite on global inflationary dynamics. The same is true for declining Chinese export prices due to subsidies on consumer goods and renewables, as well as Xi’s efforts to reduce logistics costs which may slow down costly re-shoring efforts.

The joker is how far the US and EU are willing to go to stop the flood of Chinese EVs, wind turbines etc., and how big of a deal national security concerns will become leading up to the EP and US elections. At the current pace it could get ugly..